The future of field service is going to be very different when the Smart Glasses revolution finally arrives says Pristine IO CEO Kyle Samani...

ARCHIVE FOR THE ‘future-of-field-service’ CATEGORY

May 04, 2015 • Features • Future of FIeld Service • future of field service • pristine io • Smart Glasses

The future of field service is going to be very different when the Smart Glasses revolution finally arrives says Pristine IO CEO Kyle Samani...

When Google announced the retirement of their Glass Explorer program some corners of the worldwide media denounced this as an admission of failure.

Despite huge early attention surrounding the smart glasses, the product had never quite lived up to the hyperbole and a growing number of less than sympathetic reports featuring Glass (not least to mention the widespread adoption of the newly coined term Glasshole) had meant that a shadow was being cast across Google’s latest centre piece.

For the naysayers the closing of the public beta Explorer program was a final nail in the coffin for Glass. In fact the truth remains very different.

For the naysayers the closing of the public beta Explorer program was a final nail in the coffin for Glass. In fact the truth remains very different.

What Google have done however, is take a step back from the world of the consumer and the increasingly blurred lines of fashion and technology and turned far more of it’s attention to the world of business.

An obvious, yet intelligent move given that a) the potential application of Smart Glasse is massive within industry – especially in field service and b) no one product has truly been able to meet the needs of and exploit the massive potential of wearables in field service.

Of course having the hardware is great, but to unleash the real power of such a device we need dedicated apps. For that we need developers that truly understand the audience they are working for.

So Google established the Glass at Work program.

A program where they selected the brightest and the best development companies working on Glass and gave them the support needed to help them flourish.

It’s a select group with only ten certified Glass at Work partners listed by Google currently. One of those companies is Austin based Pristine.io and to find out more about what the next chapter holds for Glass (and other similar products) in field service, we caught up with their CEO Kyle Samani.

“Pretty much the moment Google announced Glass that’s when I had my Eureka moment – I thought that’s what I’m going to go and do.” - Kyle Semanie, CEO, Pristine IO

Indeed Samani has the credentials to do well. As mentioned in the introduction, an understanding of the end-users that Pristine’s product is designed for is a large factor in their potential success and Samani whose background prior to launching Pristine was in the design and development of EMR systems for healthcare organisations was certainly well placed to step up to the plate

“I studied finance at NYU and I’ve been programming ever since I was a kid. I’ve always been at the cross section of business and technology” Samani explains.

So what led him to launching Pristine? Is it a case of being the right guy at the right time in the right place?

“Pretty much the moment Google announced Glass that’s when I had my Eureka moment – I thought that’s what I’m going to go and do.”

He admits “Someone was going to go out there and make the software to make this thing useful for the enterprise and I was dead set from the moment I saw it that it was going to be me.”

And it certainly seems that Samani has getting things right so far as his fledgling company has rapidly grown in the two years since inception.

Pristine now has over 20 employees and perhaps more importantly over 30 customers. Also whilst a background in medical systems provided a natural opening for Pristine, their customers are not confined to this space.

Whilst they exploited a niche within the healthcare sector, it was soon apparent that within the horizontal sector of field service there lay a far greater prize

As Samani explains “Our customer base is pretty broad, it does include healthcare but it also includes a lot of other companies outside of healthcare as well.”

“For example right now we are working with a large manufacturing company that produces conveyor belts, so big heavy industrial machinery, and those guys are seeing a huge amount of potential in the platform. We’re also working with companies now in the auditing space within food production for example.”

He continues outlining the variety of companies that could benefit from adopting Smart Glasses into their work-flow.

“Basically we’re seeing adoption of our technology in any environment where you have heavy equipment that if it’s not functioning, it’s going to effect the profit of the business operation. From lab diagnostics in a hospital to packaging equipment in a factory.”

“We even have one company we are working with in construction and for them a big bottleneck in terms of getting their work done is just getting an architect out on site.”

“So they are using our technology to replace the six hour flight and five hour drive. That’s essentially wasted time and expense for them but now they can have a guy on-site with a pair of smart glasses and an architect dialling in remotely avoiding the wastage”

Be social and share this feature

May 01, 2015 • Features • aston university • Future of FIeld Service • Servitization • tim baines

The world of manufacturing is getting ready for one of the most significant changes since the industrial revolution. Servitization is coming and amongst those leading the charge is Professor Tim Baines of Aston University. We're pleased to welcome...

The world of manufacturing is getting ready for one of the most significant changes since the industrial revolution. Servitization is coming and amongst those leading the charge is Professor Tim Baines of Aston University. We're pleased to welcome him to the list of field service news columnists and here in this first article he gives us an introduction to this complex yet fascinating and important topic...

The world once seemed simple; manufacturers made things and services companies did things for us. Today, increasing numbers of manufacturers compete through a portfolio of integrated products and services.

This is a services-led competitive strategy, and the process through which it is achieved is commonly referred to as servitization. Celebrated exponents of such strategies include Rolls-Royce, Xerox and Alstom; all offer extended maintenance, repair and overhaul contracts where revenue generation is linked directly to asset availability, reliability and performance.

Servitization is much more than simply adding services to existing products within a few large multi-national companies. It’s about viewing the manufacturer as a service provider that sets out to improve the processes of its customers through a business model, rather than product-based, innovation. The manufacturer exploits its design and production competencies to deliver improvements in efficiency and effectiveness to the customer.

Manufacturers have traditionally focused their efforts on product innovation and cost reduction. Companies such as Porsche and Ferrari are celebrated for bringing new and exciting designs into the market, while companies such as Toyota are held in awe for their work with Lean production systems. These successes foster a perception that the only way for manufacturing to underpin competitiveness is through new materials and technologies, faster and more reliable automation, machining with more precision, waste reduction programmes, smoother flow of parts etc.

Manufacturers have traditionally focused their efforts on product innovation and cost reduction. Companies such as Porsche and Ferrari are celebrated for bringing new and exciting designs into the market, while companies such as Toyota are held in awe for their work with Lean production systems. These successes foster a perception that the only way for manufacturing to underpin competitiveness is through new materials and technologies, faster and more reliable automation, machining with more precision, waste reduction programmes, smoother flow of parts etc.

Competition through services

Services offer a third way to compete. This is not an ‘instead of’ or ‘easy option’ for companies that are struggling to succeed. Indeed, delivering advanced services can require technologies and practices that are every bit as demanding as those in production. Neither do they require the manufacturer to abandon its technology strengths; instead it can build on these to help to ensure long term and sustained benefits. Consequently, there is a growing realisation that such services hold high value potential.

Conventional manufacturers can struggle to appreciate the value of services, seeking such simple explanations of servitization that they fail to appreciate potential benefits.

Servitization is a similar paradigm shift. The word ‘service’ can be used in different ways. It can refer to how well an action is performed – “that was good service” – or to an activity, like maintenance, spare parts provision and so on. Servitization relates to this second interpretation; activities that a manufacturer can perform to complement its products.

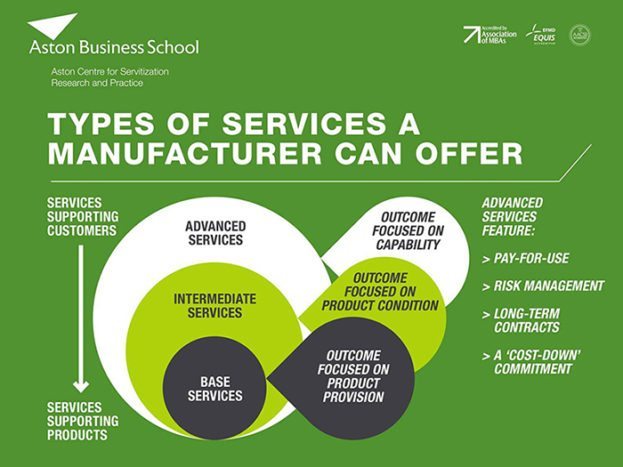

All manufacturers offer services to some extent, but some establish market differentiation through these, following services-led competitive strategies. Servitization is a term given to a transformation. It is about manufacturers increasingly offering services integrated with their products. Of these, some manufacturers choose to servitize by offering an extensive portfolio of relatively conventional services, while some move almost entirely into services, largely independent of their products, by providing offerings like general consulting. Others move to deliver advanced services.

Advanced services are core to servitization. Xerox’s ‘Managed Print Services’ is one example; rather than simply selling equipment, the company offers ‘document solutions’ to customers. For a typical customer, such as BA, Xerox provides project management, implementation of new technology, and management of third parties.

There are various types of advanced services, and a variety of terms is used across industry to describe these (e.g. availability contracting, performance contracting, managed services, solutions). However the outcome of these contracts is, invariably, a capability for a customer to perform a business function or process.

This is distinct from conventional services where the outcome is product ownership and maintenance of an asset’s condition. Particular contracting features are often coupled to advanced services.

There are four key features; the first three of which are relatively widespread: Pay-for-use revenue payment: pay-per click, pay-as-you-go, power-by-the-hour etc. are all terms used to refer to advanced services. For instance, in its contract with Xerox, Islington Borough Council receives a ‘click charge’ each time a document goes through a machine.

MAN Truck and Bus UK has 10,000 vehicles under contract, and expects this to grow by 50% over the next three to five years, to represent £200million of business.

When these features are coupled with the principle of delivering a capability, contracts become sophisticated and demanding. Many existing contracts are relatively large, which is perhaps part of their appeal to OEMs. MAN Truck and Bus UK has 10,000 vehicles under contract, and expects this to grow by 50% over the next three to five years, to represent £200million of business. The Heart of England NHS Foundation Trust’s five-year contract in its pathology laboratory is valued at £20M per year.

Advanced services are however not only for large organisations. They can hold high-value for manufacturers big and small. They can help strengthen relationships, lock-out competitors, and grow revenues and profits and this is why servitization can be a sustainable business model for manufacturers of all sizes.

Want to know more - why not attend the Servitization Spring Conference in May 18th - 19th Click here for more information

Be social and shared this feature

Apr 28, 2015 • Features • Advanced Field Service • Future of FIeld Service • research • Research

Our exclusive research project sponsored by Advanced Field Service looks at the types of solutions being used by Field Service companies in 2015 and how those companies select the right solutions to meet their needs. Across the next four weeks we...

Our exclusive research project sponsored by Advanced Field Service looks at the types of solutions being used by Field Service companies in 2015 and how those companies select the right solutions to meet their needs. Across the next four weeks we will present you the findings of this research...

There is also a white paper accompanying this series, with even further insights, which you can download here

Field Service News has recently completed a research project, sponsored by Advanced Field Service, into what types of mobility tools are being used by field service companies. What types of hardware are most commonly being selected for our field engineers? What software is being used out in the field? How are companies selecting the right solution for their engineers?

What feedback are those engineers giving? And what actual benefits are being delivered through digital mobility solutions?

In total 122 field service professionals responded to our survey which ran across February and March with respondents from companies with mobile workforces ranging from less than ten field engineers through to over 801 engineers and with an even number of representatives across the spectrum with no obvious spikes, the research offers insight into trends across field service as a whole.

Types of devices being used in the field

It is perhaps no surprise by now that most companies are using some form of digital device.

We have been going through a digital revolution across the last decade and no industry has felt the impact of this change as keenly as field service.

Indeed out in the wider world of industry the emergence of Enterprise Mobility as a definable, and eminently sizeable industry that will ultimately dwarf the size of the field technology sector considerably, has now firmly taken root. However, the field service industry, which has more complex needs than it’s younger cousin of Enterprise Mobility, is also a far more mature market in general.

In fact our research indicates that the majority of companies are using a mix of differing digital devices, with 46% stating this is the case. This would make sense as many field service organisations are now in their second, third or even fourth generation of digital device being rolled out to their field engineers.

However, when it comes to those companies that have rolled out just one device to their mobile workforce the results revealed some further insight into the trends now appearing amongst field service companies.

“It appears the rumours of the death of the laptop have been greatly exaggerated”

Of course every action has a reaction, and the rapid growth of smart phones as a tool for field service engineers has resulted in an equally rapid decline in the use of PDAs. In fact now just 5% of companies are using these devices - the smallest percentage of any device being used within the field.

One myth however that the research helps debunk is that Tablet computing his having a similar impact on the laptop sector as smartphones are having on PDAs.

Whilst it seemed at one point that the trend for tablet computing would see the laptop being edged out of both the consumer and rugged markets it appears the rumours of the death of the laptop have been greatly exaggerated.

In fact our research outlines that in terms of the devices being used on there own, both tablets and laptops have an equal share of the market at 14%.

However, we should also consider the fact that of those companies who provide more than one device to their engineers, a large proportion of companies are likely to offer a laptop as one of those devices, largely due to the fact that having a built in keyboard makes any significant manual input much easier.

So whilst it is likely that ultimately the traditional laptop will become replaced by the convertible or even the detachable laptop, the keyboard remains an important part of the field engineers mobile technology kit.

The last few days of pen and paper

What the research presents clearly is that the masses in field service have moved towards the new digital dawn.

There are of course in any industry sector, laggards that remain behind the trend.However, when it comes to the application of mobile technology amongst field engineers this group (i.e. those using no digital medium) now stands at just a nominal 3%.

Not only the is the group now just a very small minority, but our research also indicates that this group is potentially set to disappear completely within the next twelve months.

Of those companies still using pen and paper 100% stated they are considering moving to a digital mobile platform within the next twelve months.

The reasons for this are of course clear, as are the benefits of moving to any digital medium, including increasing productivity and streamlining a field engineers work-flow.

The fact is that those companies still relying on pen and paper are in danger of falling significantly behind their competition.

In fact of those companies still using pen and paper 100% of the respondents admitted that they felt they were at a disadvantage, with 50% stating that they felt that disadvantage was significantly impacting their ability to remain competitive.

Want to know more? Download the exclusive research report for free now!

Click here to read the second part of this research report coming next week which will look at Wearables, Rugged vs. Consumer and BYOD...

Find out more about Advanced Field Service in the Field Service News Directory

Be social and share this feature

Apr 28, 2015 • Features • Future of FIeld Service • Service Community • Servitization

Held at Fujitsu Stevenage, this event brought together 35 service professionals from around the country who listened to and discussed four excellent presentations covering various aspects of Outcome Based Services.

Held at Fujitsu Stevenage, this event brought together 35 service professionals from around the country who listened to and discussed four excellent presentations covering various aspects of Outcome Based Services.

The excellent speaker this time around were:

- Veronica Martinez a globally eminent researcher in the area of Servitisation, presented an overview of the research she has been doing with the Cambridge Service Alliance. She told us how some of the worlds leading brands have approached developing Outcome Based Services, giving an exceedingly deep insight into the change process. Brilliant for any manager working on service transformation!

- Alex Bill gave his perspective of developing Outcome Based Service at the coal face. As a service professional in a major Power Generation OEM, he gave us insights into how the business model to make money is not as simple as just selling a service.

- Des Evans, the Ex CEO of MAN UK gave us the business perspective on servitisation, with insights from his 23 year journey to grow the business from £55M to £550M. It was a must ‘hear’ for anyone selling service concepts to their board.

- Chris Farnath Director International at Allocate Software, shared his own personal journey in leading business change toward outcome based services in the IT/Software world. Again incredibly useful to understand how he is approaching the ‘messy’ challenge of service transformation.

Thanks to all the participants for a great networking and discussion event

For a personal perspective on the event, read Martin Summerhayes’ account below which is also published in his personal blog.

Service Community Conference - Outcome Based Services

[quote]“The purpose of a business is to get and keep a customer. Without customers, no amount of engineering wizardry, clever financing, or operations expertise can keep a company going.” ― Theodore Levitt

The first Service Community event for 2015 was held this week. There are two Service Community conferences that are held every year. They were first started by a wonderful consultant and friend, Steve Downton, many years ago and have continued to be popular and thought provoking events. Unfortunately, Steve lost his battle with cancer last year and a number of the core members of the community [including myself] decided to keep the event going - as much in Steve’s memory - as well as it gives a fantastic, open forum to share ideas, the latest thinking and case studies from the world of Services.

One of the key differentiators to other events, is that it brings together service practitioners to discuss and share ideas, changes in markets, share best practices and case studies. It is not an event where people come to try to sell products, services or companies - this is not what the Service Community is about.

Here were delegates from the widest spectrums of industries, including: Power Generation, Academia, Construction, Cancer Technology Treatment, Sports Goods Technology, Logistics, Digital Photography, Soft Drinks Manufacturing and then the traditional IT and IT Services businesses.

What brought us together for this conference? The theme was “Outcome Based Services (OBS)”.

A number of points struck me during the series of four presentations and follow up discussions during the event. Obviously, the first point to mention, is what on earth are Outcome Based Services? The following points highlight the key elements of Outcome Based Services:

1. Predetermined results and predictable costs defined in agreement with the customer and are a reflection of the customers business:

One example quoted related to the transport industry. The traditional approach is to pay separately for the truck, servicing, tyres, risk certification and then the fuel and driver. The customer then has to try to find the best deals for each of these elements. In addition, something I did not know is that a truck is only productive 25% of the time i.e. actually on the road delivering products and goods and hence making money. The OBS approach is to provide the vehicle and charge the customer on “price per kilometre”.

2. Protection of the client’s investments:

One of the concepts discussed was leasing the product and having all of the associated services wrapped around it in a single charge. For example, the Rolls Royce model used to lease aero-engines which was shared at a previous event.

3. Short, medium and long-term savings adapted to changing client needs:

One example was based on the savings from the production of electricity for the national grid using gas turbines. The customer could pay for either short term availability [how quickly you can turn on/off a turbine], medium term savings from the use of fuel, or even longer term savings from the ability to have upgrades build into the outcome based charging model which means the product stays in useful 2-5 years longer.

4. Use of methodologies, tools and processes to deliver outcome commitments and continual productivity improvements:

The presentation from the University of Cambridge Service Alliance included a Service Strategy model - with examples where different customers had started the journey to “OBS”, In addition, the presenter talked about you might have to segment your customers as only some would be interested in OBS; that Risk Management and how you would deliver exactly what was required [the example given was the tonnage of rock removed by an explosives company] was critical and even giving away low margin services for “free” to be able to maintain a “sticky” relationship with your customers.

5. Operational excellence through the use of best practices, regularly reviewed to ensure their long-term applicability:

The final example was a software company that realised that the current, traditional approach of implementing software solutions was not meeting the needs of their customers and has started on a journey to change the complete services landscape across their organisation to focus on “Adoption”. They had attended and worked with the leading industry experts, learnt the best practices and were implementing them in their organisation. The key to their success, though, was that the entire Operations Board of the company was behind the move.

My overall definition of Outcome Based Services based on the presentations and examples given would be:

Outcome Based Services are where you as the Service Provider, COMMIT to providing high-quality; customer defined and reflective of THEIR business; services; aligned with predetermined service levels and fixed prices, where there is a Shared Risk and Reward strategy in place for both supplier and customer.

Be social and share this report

Apr 27, 2015 • Features • Future of FIeld Service • MAC Solutions • Microsystem • Nick Frank • IoT

Have you ever had a great business idea, and found yourself saying ‘Oh that’s just a bit beyond our capability’. Shame, as you have already talked yourself out of it before you have even started!

Have you ever had a great business idea, and found yourself saying ‘Oh that’s just a bit beyond our capability’. Shame, as you have already talked yourself out of it before you have even started!

But if a project seems a little too big for your business, perhaps give it a second chance by exploring partners that can make up for your capabilities gap. Service Management expert Nick Frank, Principal at Frank Partners explains more...

Many businesses utilise local partners or agents to sell and service their products in regions outside their organisations reach. This arms length type relationship is OK until you start wanting to develop more advanced service offerings, which may require a far deeper integration between the product side of your company and the customer facing service operations.

Value propositions such as uptime guarantees, vendor managed inventory or outcome based services require far more interaction between the manufacturer the agent and potentially multiple partners.

Take the fastener manufacturing company that was asked by a major Automotive OEM to supply every single nut, bolt, rivet, screw and clip for a particular car platform. Rather than supplying 10 part numbers, they now had to supply 450 most of which they now had to buy-in! How do you go from manufacturer to a ‘just-in-time’ delivery partner with a global supply base in just 3 months?

Their solution was to use a 3rd party logistics provider to move parts from all over Europe to a point of fit in the factory, while they focussed on Application Engineering Services, Purchasing and Programme Management. They challenged their mind-set and built a supplier ecosystem that included many of their competitors.

As the business developed some competitors even became key customers and suddenly relationships were not quite as simple as before. It shows that with a bit of creativity, an advanced service offering can be delivered that goes beyond the initial core capabilities.

So how can an organisation provide solutions for complex customer business problems that at first sight appear to be beyond their capability?

Recently I worked with a small UK SME who embarked on creating an ecosystem to deliver an IoT technology platform that enables smaller equipment suppliers to deliver remote services such as diagnostics and upgrades. MAC Solutions is a £2M+ UK supplier of industrial router solutions.

This went beyond the router and cloud technologies it currently supplied and involved the integration of Historians, Alarm Management Analytics and other new data technologies.

As they brought the partners together, it became clear that inter-relationships became more complex and could not be managed as a traditional customer/supplier discussion. They developed a framework that helped them think clearly through the process of developing their service solution.

It essentially linked together standard business tools that enabled clearer business thinking through 4 key steps:

- Understand the Value Chain and the market: The basic business analysis that should be in gaining a deep insight into the markets, customer value and the current business context. This understanding becomes very important when it comes to agreeing pricing mechanisms with different partners

- Define the complex problem to be solved and the ecosystem solution: in other words the basic building blocks of the solution, so that a clear vision, mission and strategy can be articulated and actioned. This involves clearly defining the Business Opportunity, Value Proposition, Product Service Solution and the Roles & Responsibilities within the partner ecosystem.

- A clear plan of how to execute and develop the solution: For example develop a detailed business plan to drive the allocation of resources and actions. How will you use pilot projects to develop your solution? Develop the Value Delivery Model that defines the commercial interactions within the ecosystem. This would cover the sales model, delivery model, people and competencies, customer experience, organisation, partnerships and contracts, pricing, revenue sharing schemes and procurement

- Test for Resilience: Develop mechanisms for ensuring that the business plan is resilient in terms of business risk and partner/customer fit

The framework they developed, undoubtedly helped them move through the complex process of developing a network of partners that can deliver results. The result has been that MAC-Solutions were able to pilot their proposition with a supplier of washing systems for rail networks.

Their story shows how it is possible for even small organisations to develop service propositions that appear to be beyond their capability by developing an ecosystem of partners.

MAC-Solutions will be telling the story in more detail at the Spring Servitisation Conference to be held at Aston Business School in May 2015.

Be social and share this feature

Apr 15, 2015 • Features • Future of FIeld Service • millenials • infographic • servicemax

We’ve all seen the statistics on how Millennials are set to dominate the workforce by 2020. Individual companies and entire industries are starting to cater to their requirements - from collaborative business centres and “social lobbies” for...

We’ve all seen the statistics on how Millennials are set to dominate the workforce by 2020. Individual companies and entire industries are starting to cater to their requirements - from collaborative business centres and “social lobbies” for networking/relaxation, to rooms equipped with the latest technology. Businesses are embracing this new generation, and harnessing the power of their sheer numbers.

It’s been said that this generation is needy, entitled, narcissistic, and often tough to manage, but they can also bring a new element to business, representing a driving force and competitive weapon that can be used to differentiate your organisation, strengthen the connection between you and your customer, and further the revenue and bottom line growth for your company.

Their attributes are actually a good fit for a career in the field service industry. Our entire civilisation now depends on field service technicians to maintain the very machines that keep our world running. Given the profitability potential that field service now has to drive meaningful revenue in a fledging economy where product shelf life is being extended rather than replaced, a career in field service gives Millennials the potential to both make money and make a difference.

The infographic below published by ServiceMax outlines how to the service industry can appeal to Millennials as a career path, and the changes in motivational drivers.

Be social and share this feature

Apr 13, 2015 • News • Advanced Field Service • Future of FIeld Service • M2M • machine to machine

Service management organisations could miss out on vital business intelligence, lucrative new revenue streams or fail to meet rising customer demands unless they embrace machine-to-machine (M2M) technology. These are the findings of a new white...

Service management organisations could miss out on vital business intelligence, lucrative new revenue streams or fail to meet rising customer demands unless they embrace machine-to-machine (M2M) technology. These are the findings of a new white paper commissioned by service management software provider, Advanced Field Service (Advanced).

The worldwide M2M technology market is forecast to grow to £30 billion by 2018* and is set to revolutionise the service management industry. However some businesses remain cautious about adoption due to limited time and resources, cost pressures and cultural resistance.

A recent survey[quote float="left"]“There is some confusion as to how M2M interplays with other technologies such as The Internet of Things, cloud, big data and mobile. While there is no clarity about what M2M is, and the benefits it offers, adoption rates will be slower than anticipated.

conducted by Advanced highlights that only 43% of businesses are currently using M2M. Just over a quarter (26%) of respondents revealed they are considering M2M but in contrast 31% said they had no plans to do so.

Greg Ford, Managing Director of Advanced Field Service, says, “There is some confusion as to how M2M interplays with other technologies such as The Internet of Things, cloud, big data and mobile. While there is no clarity about what M2M is, and the benefits it offers, adoption rates will be slower than anticipated.

“Many service organisations will need to wait for manufacturers to introduce the capabilities of M2M before they can take full advantage of it. For those who serve multiple manufacturer products, this can make planning and gaining access to data more difficult.”

M2M is effectively a subset of the Internet of Things and wirelessly connects machines, devices and equipment to collect and transmit data such as location, movement, temperature and environment. Typical solutions enable the remote tracking of a business’s field-based assets, ‘smart metering’ to monitor and control energy and utilities and telematics systems to enhance service delivery performance through automated processes.

Ford comments, “M2M technology provides valuable insight into the performance of equipment, vehicles and field engineers. With this crucial business intelligence, organisations can shift from reactive to predictive service, ensuring issues can be identified and resolved more quickly to meet rising customer expectations.

“M2M can also transform efficiency levels and increase profit margins. With rising costs and fierce competition continuing to impact the service industries, organisations who choose to overlook this technology may suffer a detrimental impact to their bottom line.”

Advanced Field Service’s integrated service management solutions enhance business intelligence for companies which provide installation, service or maintenance via a field or site-based workforce. Its Siclops system enables organisations to improve productivity, reduce administration costs and streamline scheduling processes.

Mar 19, 2015 • Features • Aftermarket • aston university • Future of FIeld Service • Lely • manufacturing • IFS • tim baines

At the recent AfterMarket conference in Amsterdam Field Service News Editor, Kris Oldland hosted a panel debate with three speakers key to servitization; Professor Tim Baines, Aston University a leading proponent of the movement, Brendan Viggers,...

At the recent AfterMarket conference in Amsterdam Field Service News Editor, Kris Oldland hosted a panel debate with three speakers key to servitization; Professor Tim Baines, Aston University a leading proponent of the movement, Brendan Viggers, Product and Sales Support for IFS Aerospace & Defence division who has worked closely with a number of companies such as Emirates on moving towards a servitization model and Koen D’Haeyer, Global Manager Service Development & Technical Services Lely who had been through the journey himself with Dutch Farm Technology company.

In the first part of this feature we looked at whether servitization was limited to just large size companies and how to manage the change involved in moving to such a radical new approach. Here in the final part of this feature the debate continues....

Kris Oldland: There is a point there that you touch on briefly about not just getting the buy in from the internal teams but also from the customer. Data can play a significant part in servitization and that presents a challenge in it’s own right, as data is very precious currently. How can we overcome that and encourage our customers to let us access their data?

Koen Dyaeyer: To start I’ll mention one thing, there is an aspect on this benchmarking data with your customers which is of course, that you are obliged to do this anonymously that is clear. You can tell the a customer ‘look this is your data this is the rest of the market and this is the variation’ but you cannot be open to all extents.

But the value is not in knowing exactly who is doing what, the value is in comparing yourself with others and knowing what to learn, and how to then improve.

I would say twenty to thirty percent may adopt really quickly, really embrace it and are immeditely fond of the concept, another twenty to thirty percent will be lagging – it is not in their mindset and then the part in the middle is where you have to push

Brendan Viggers: Certainly in the defence market the classic contracting model is performance based logistics where the OEM is providing a platform and then the through life support of the platform as well, so all the servicing that goes with it and they will then offer a SLA or guarantee the fleet availability for 80% of that time.

What we are finding is there is a need for partnership between the OEM and the customer. Because the OEM needs to know how the customer is driving that vehicle. If he is taking that tank and forcing it across a plain over the bounds of normal operational use then it’s going to cost that OEM more to service it. So can be a win-win but if you want that platform you need to be prepared to operate within acceptable bounds.

Koen Dyaeyer: To add to Brendan’s point there I would add that in our case we are looking for the win-win-win because we are in between but if we focusses on the win-win-wins we can really drive forward.

Tim Baines: This debate about ownership of data has been going on for over 10 years. To my mind its the use of the data that is important. I’ve seen it in Xerox’s case where they will turn around and say OK the contract price is this for an advanced services contract on print management but if you let us share that data and use that data it’ll come down to this.

Audience Question: What would you say are your most important KPIs to actually monitor and drive your service business today?

Koen Dyaeyer: The most important group of KPIs are the service profitability KPI’s we have data on overall revenues and data on cost indicators. We cannot always be exact with th eservice cost indicators to the penny but we know what it is likely to be. So the service profitability is a major KPI.

The first question we ask in every technical assessment is what type of customer do you think this is and also is he satisfied? So we link that data to understand the relationship of data to customer satisfaction.

Then for the operations we also have the performance KPIs of the product so mean time between failure, mean time between breakdown, some performance indicators specific to our industry so number of failed milkings for example that help us see if the farm management is running smoothly. So performance, customer satisfaction and service profitability – these are the three main KPI group we use.

Kris Oldland: Have these KPIs evolved as you have moved through this process of servitization? Have they evolved as you gather more data and therefore Insight into your customers?

Koen Dyaeyer: Actually we started with maybe 8 or 10 basic KPIs and what we started to get excited about was the analysis we could do with them. We were able to look at the years of technical experience and see how that aligned to customer experience and service profitability. We learned a lot out of that initial process and then some new KPIs grew out of it .

Tim Baines: I may have seen something slightly different in some of the companies that I have looked at. A quote that comes to mind is by Henry Ford who said profit is a result of service. Therefore when I look at people like Alstom the number one KPI is around customer experience.

That means the customer experience, which in their instance would be the amount of time a customer is waiting because a train has failed to show up, that customer experience is the number one KPI.

For Alstom that’s key because it relates directly to the customers key core business process, which is about moving people. Then there are KPIs around the customer experience when somebody is onboard the train and so on. It’s the manufacturer that then translates those to mean time to failure etc.

What is very interesting to me coming from a world of production, where the main KPIs were cost, quality and delivery and everything was around that then moving to the service world where KPIs are centred around the business processes of the customer

Audience Question: I am understanding this correctly that the fourth industrial revolution is about re using our IP and industrial assets to serve customers better?

Tim Baines: I think that we are looking at a very special form of organisation. What is particular about the technology innovators you see here is that if they have the internal procedures in place to capture how the product is performing in the field and then feedback to the design process so the product becomes better suited for application, then that innovation loop is what is distinctive about the manufacturing companies and is different to technology innovators.

Ultimately it means language like through life support are actually a characteristic of the old product mentality, we’re talking about a capability being delivered. Indeed even the notion of After-sales service is a product based concept because we are thinking of the notion of producing something selling it transactionally and then after sales.

Another point to make is that we talk about servitization from the point of view of a manufacturing company, a company that’s got technology innovation capabilities delivering advanced services. But we also have the phenomena of companies which are service companies, technology integrators, developing their ability to technology innovate.

So there are two ways that servitization can arise. Predominantly we talk about a move from manufacturers to manufacturers that deliver service but we can also talk about service providers developing their abilities to redesign products.

be social and share this feature

Mar 11, 2015 • Features • Future of FIeld Service • Glass • Kyle Samani • pristine.i.o • wearables • Smart Glasses • Smartwatches

There were some big claims at the start of 2014 around the impact that wearables would have both in business and in the mainstream and with this weeks announcement of the now imminent AppleWatch launch similar noises are being made as fashion and...

There were some big claims at the start of 2014 around the impact that wearables would have both in business and in the mainstream and with this weeks announcement of the now imminent AppleWatch launch similar noises are being made as fashion and technology come ever closer.

But Apple has a mountain to climb if they are to be the brand that finally cracks the consumer smartwatch market.

Rewind back a year and we were being told this was the year of the wearable. Just one year later and there is a distinctly different attitude doing the rounds, one that not only lacks the optimism of last year but also has a defiant hint of those pessimistic ‘I told you it wouldn’t work’ types.

Rewind back a year and we were being told this was the year of the wearable. Just one year later and there is a distinctly different attitude doing the rounds

Yet Glass isn’t dead, far from it and we’ll come back to that in a moment.

But first, let’s look at the wider question around wearables and why 2014 didn’t live up to the hyperbole as being the ‘Year of the Wearable”.

With high profile wearable launches from Samsung, Apple and of course Google being widely anticipated for 2014 it was with much anticipation that Wearables which had been touted as the next big thing from as early as 2008 would finally breakthrough and gain mass appeal in the consumer market.

Yet the fact is that we as consumers just weren’t ready.

Whilst 75% of consumers are aware of wearable technology, just 9% actually had any desire to purchase

However, whilst there is a clear lack of desire to be dubbed a ‘Glasshole’ by adorning a wearable device, this doesn’t equate to why there has also been little adoption in the world of enterprise. Lets be honest hi-vis jackets aren’t exactly high-fashion (well not since the early nineties for those ex-ravers out there) but I highly doubt that has halted their sales in the various industries they are required.

Personally, I think there are two key reasons why we have not seen wearables become popular in a working environment as yet.

Firstly in all the excitement and hyperbole surrounding wearable computing we’ve perhaps overstated the impact and the sheer power of a wearable device. One common misconception I hear around smart watches in particular is what is the point when I can do everything that the watch offers on my smartphone?

This is a fundamental flaw in the thinking around smartwatches and wearables in general. Whilst they offer much of the same functionality they are not devices to replace your phone or tablet, they are companion devices to enhance the productivity of the your phone. And in field service in particular such enhancements can be particularly powerful.

In an environment where working hands free is of a huge benefit, then the ability to have a phone conversation without having to have one hand restrained holding your phone can be very advantageous.

‘Well that could be done using a bluetooth headset’ some might say. Yes it could. However, dialling a number isn’t, whereas it is via a smart watch (often via voice activation). Another good example of smartwatches being put to good use in field service would be to take photos of any issues or fixes etc.

So again we here the cries of ‘well I can do that on my phone – is it so hard to take out my phone out from my pocket to take a photo’.

When we come down to it isn’t that the point of technology to make things quicker and easier?

However, if we are talking about using wearables as a true companion device then perhaps a better example would be using the two devices in tandem.

For example lets say an engineer believes that the problem lies at the back of a piece of equipment that is inaccessible. The only solution would be to move the equipment to check.

However, an engineer with a smartwatch may be able to position the watch around the device whilst viewing the footage on their smartphones screen. A quick visual check using this combination of technology could confirm whether or not this is where the issue lies, saving the hassle of unnecessarily moving the equipment, speeding up the engineers workflow.

There are already a number of apps developed that allow this functionality.

However, none are designed with this specific application in mind and herein lies what I believe to be the second reason we’ve yet to see smartwatches make an impact in industry. Simply a lack of developers designing apps specifically for specific business niches.

There have been some attempts, most notably ClickSoftware’s Shift Expert release on Saleforce Wear, but for wider adoption we need more apps.

And this is where we return to Glass being still very much alive. Whilst in some corners Google’s removal of Glass from public sales is seen as an acknowledgement of failure, the truth I believe is very much different.

Whilst there have been reports that developers for consumer apps are losing interest in creating apps the list of Glass Certified Partners has increased with apps being developed for a wide variety of industries.

One of those Glass Certified Partners is Pristine.io who despite only coming up to their second year have already grown from start up to a $5.5M venture financing backed company with 20 staff in their very short lifetime.

Google have publicly said they are actively investing in the enterprise version of Glass

Commenting on the future potential of Glass Kyle Samani, Founder of Pristine.io said.

“Google have publicly said they are actively investing in the enterprise version of Glass and we are one of the very few certified Glass Enterprise Partners, we work with Google very closely both with engineering and business process around Glass, Enterprise and the future of the Glass product and we are very excited by where it’s going”

“Google is supporting us with hardware, software with engineering support and business support where we need and that’s been great.” He added

So it seems business is where Google’s core focus is, which makes sense as the benefits of smartglasses for Field Service is potentially massive, particularly with companies such as Pristine.io developing applications designed for purpose.

It may take a little longer than at first expected but Glass is far from dead, and as more apps are developed for wearables devices the more wearables will become integrated into our working lives. I firmly believe it will happen, we just all got a little too excited too early.

Field Service News is published by 1927 Media Ltd, an independent publisher whose sole focus is on the field service sector. As such our entire resources are focused on helping drive the field service sector forwards and aiming to best serve our industry through honest, incisive and innovative media coverage of the global field service sector.

Field Service News is published by 1927 Media Ltd, an independent publisher whose sole focus is on the field service sector. As such our entire resources are focused on helping drive the field service sector forwards and aiming to best serve our industry through honest, incisive and innovative media coverage of the global field service sector.

Leave a Reply